Hotels & Accommodations

Sinclairs Hotels Faces Financial Challenges Amidst Strong Long-Term Performance

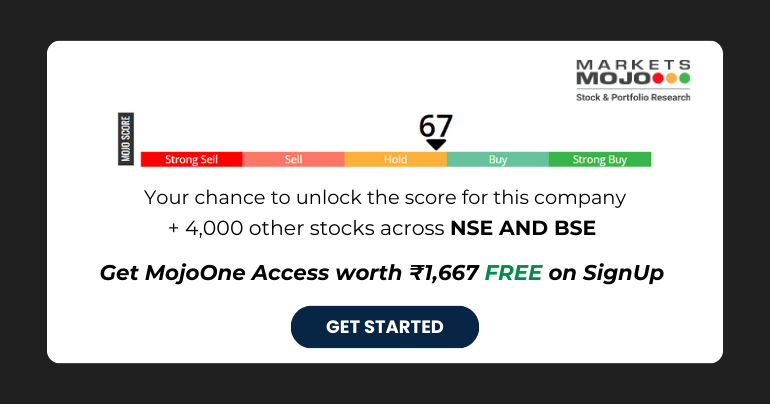

Sinclairs Hotels, a microcap player in the Hotels & Resorts industry, has recently undergone an evaluation adjustment, reflecting changes in its underlying financial metrics and market position. The stock’s technical indicators have shifted, with the technical trend moving from a mildly bearish stance to a sideways position.

In terms of performance, Sinclairs Hotels has experienced a notable return of 126.57% over the past three years, significantly outpacing the Sensex’s return of 49.96% during the same period. However, the company has faced challenges in the short term, with a year-to-date return of -17.88% compared to the Sensex’s 4.63%.

Financially, the company reported a decline in key metrics for the quarter ending March 2025, with a 31.19% drop in profit before tax and a 28.9% decrease in profit after tax. Additionally, the company’s return on capital employed (ROCE) has reached a low of 14.26%, and its return on equity (ROE) stands at 12.1%.

Despite a low debt-to-equity ratio, the valuation appears expensive, with a price-to-book ratio of 4.5, indicating that the stock is trading at a premium compared to its peers.

Hotels & Accommodations

Wyndham Hotels & Resorts Shares Jump After Q2 Earnings Beat Expectations, What You Should Know Now

Thursday, July 24, 2025

Wyndham’s stock rallied 4.3% in after completing its second quarter, which blew past Wall Street estimates. The hotel franchise powerhouse posted adjusted EPS of $1.33, above analysts’ $1.16 EPS tree.

Much of this performance was driven by an increase in development activity and continued resilience in our ancillary revenue programs, which combined to offset the softer U.S. demand backdrop that Wyndham encountered.

Revenues Reflect Resilient Business Model

Quarterly revenue totaled $397 million, exceeding the consensus estimate of $386.64 million. The strong performance, not surprisingly, showed Wyndham’s ability to expand in a changing travel landscape with a diversified revenue model capable of working well while different regions ebb and flow.

One of the main factors of a volume increase came from ancillary revenue which jumped by 19% year over year. Those gains, offered through services that go beyond mundane room bookings, acted as a buffer against the 4% year-over-year decline in U.S. revenue per available room (RevPAR).

International Growth And Development Pipeline Set Records

The Company’s international presence further grew with global system size increasing 4% year-over-year to approximately 846,700 rooms. At the same time, the company’s development pipeline reached a record 255,000 rooms, a 5% increase in the second quarter of 2024.

Additionally, Wyndham signed 229 new development contracts this quarter, a 40% increase over 2018. This healthy growth in the pipeline indicates considerable long-term demand and investor confidence in the expansion potential for the brand.

Strategic Focus on Higher-Margin Markets

Geoff Ballotti, the company’s President and Chief Executive Officer, noted that the company’s expansion is being fueled by its strategic focus on high FeePAR (fees per available room) markets and segments. Though not cited directly, he noted that the company is still focussed on growing its global presence, increasing its development pipeline and increasing its high margin ancillary revenues.

This methodical strategy looks like it is paying off as the company focuses on growing in markets with better profitability, while reducing exposure to markets with weaker occupancy trends.

EBITDA Climbs with Shareholder Returns on Schedule

EBITDA for the quarter was $195 million— this was 10% higher than the year ago quarter. On a constant currency basis, that was a 5% increase.

Wyndham has also shown its dedication to providing value for shareholders. The company gave back $109 million in Q2 to investors in the form of shareholder returns, comprised of $77 million in share repurchases and $0.41 of quarterly cash dividends per share. This action illustrates Wyndham’s belief in its resiliency and future performance.

Upgraded Outlook for FY2025

In an optimistic tweak, Wyndham boosted its full-year 2025 adjusted EPS outlook to between $4.60 and $4.78. Not seeing the calculation of the adjusted earnings at this time, This adjustment is as usual just a little better than the consensus estimate of $4.68, indicating a bullishness over the strength of the second half that continued into 2008.

The company also raised the bottom of its annual forecast for room growth, for which it is now forecasting a year-over-year gain of 4.0% to 4.6%. That suggests the management team is confident of continued robust development activity in its markets, despite wider macroeconomic uncertainties.

Debt Level Comfortable And Not Excessive

At June 30, 2025, Wyndham’s net debt leverage ratio remained 3.5 times—well within its target range of 3 to 4 times. This fiscal discipline enhances the company’s flexibility for future investment, growth and shareholder returns.

Market Outlook and Investor Confidence

Wyndham’s positive share price reaction to the company’s Q2 results reflects investor confidence in the company’s long term plan and the growth story. While the U.S. domestic business faced challenges, including a decline in RevPAR, Wyndham’s diversified approach with global expansion, service offerings and asset-light franchising will enable it to remain profitable.

With the strong forward momentum and sound financials, Wyndham seems to be set to keep building in the latter half of 2025.

PARSIPPANY, New Jersey—Wyndham Hotels & Resorts announced its second-quarter 2025 results. Highlights include:

- System-wide rooms grew 4 percent year-over-year.

- Awarded 229 development contracts globally, an increase of 40 percent year-over-year.

- Development pipeline grew 1 percent sequentially and 5 percent year-over-year to a record 255,000 rooms.

- Ancillary revenues increased 19 percent compared to the second quarter of 2024 and 13 percent on a year-to-date basis.

- Diluted earnings per share increased 6 percent year-over-year to $13; adjusted diluted EPS grew 18 percent to $1.33, or 11 percent on a comparable basis.

- Net income increased 1 percent year-over-year to $87 million; adjusted net income increased 13 percent to $103 million, or 7 percent on a comparable basis.

- Adjusted EBITDA increased 10 percent year-over-year to $195 million, or 5 percent on a comparable basis.

- Returned $109 million to shareholders through $77 million of share repurchases and quarterly cash dividends of $0.41 per share.

“We delivered another solid quarter growing our global system by 4 percent, expanding our development pipeline by 5 percent, increasing our ancillary revenues by 19 percent, and continuing to execute our strategy focused on higher FeePAR segments and markets, which is driving growth in both domestic and international royalty rates,” said Geoff Ballotti, president and chief executive officer. “Record first-half openings and a 40 percent second quarter increase in new contracts awarded reflect strong developer confidence in Wyndham’s powerful, owner-first value proposition. Amid a softer domestic RevPAR environment, we grew comparable adjusted EBITDA by 5 percent and comparable adjusted EPS by 11 percent. We also returned nearly $110 million to shareholders this quarter — continuing to demonstrate the value-creating power of our highly cash-generative, resilient asset-light business model. With consistent development, royalty rate, and ancillary fee growth, we remain very confident in our ability to create long-term value for our shareholders, franchisees, and team members through the enduring appeal of our iconic brands.”

Revised International Reporting Basis

As part of a recent operational review, the company identified violations of its Super 8 master license agreement in China and issued a notice of default to the master licensee. Given the operational challenges of obtaining accurate information from this master licensee and the uncertain outcome of the compliance process, beginning this quarter, the company has revised its reporting methodology to exclude the impact of all rooms (approximately 67,300 rooms as of March 31, 2025) under this master license agreement from its reported system size, RevPAR and royalty rate, and corresponding growth metrics. The company’s financial results will continue to reflect fees due from the Super 8 master licensee in China, which contributed less than $3 million to the company’s full-year 2024 consolidated adjusted EBITDA.

The company’s global system grew 4 percent, including 3 percent growth in the higher RevPAR midscale and above segments in the U.S. and 5 percent growth in the higher RevPAR EMEA and Latin America regions.

On June 30, 2025, the company’s pipeline consisted of approximately 2,150 hotels and 255,000 rooms, representing another record-high level and a 5 percent year-over-year increase. Key highlights include:

- Awarded 229 new contracts, an increase of 40 percent year-over-year.

- 6 percent pipeline growth in the U.S. and 4 percent growth internationally

- Approximately 70 percent of the pipeline is in the midscale and above segments, which grew 5 percent year-over-year

- Approximately 17 percent of the pipeline is in the extended stay segment

- Approximately 58 percent of the pipeline is international

- Approximately 76 percent of the pipeline is new construction, and approximately 35 percent of these projects have broken ground

RevPAR

Second quarter global RevPAR decreased 3 percent in constant currency compared to 2024, reflecting a 4 percent decline in the U.S. and 1 percent growth internationally.

In the U.S., second-quarter results included approximately 150 basis points of unfavorable impacts from the timing of the Easter holiday and the 2024 solar eclipse. Excluding these impacts, the company’s U.S. RevPAR declined approximately 2.3 percent year-over-year, driven by softer demand, partially offset by a modest increase in pricing.

Internationally, RevPAR results were driven by continued pricing power, offset by a decline in occupancy. The company continued to see strong performance in its EMEA and Latin America regions, with year-over-year growth of 7 percent and 18 percent, respectively, reflecting robust pricing power in both regions. The company’s Canada region grew RevPAR by 7 percent, reflecting increased room nights from Canadian guests. In China, RevPAR decreased 8 percent year-over-year, reflecting a decline in occupancy and continued pricing pressure.

Second-Quarter Operating Results

The comparability of the company’s second-quarter results is impacted by marketing fund variability. The company’s reported results and comparable-basis results (adjusted to neutralize these impacts) are presented to enhance transparency and provide a better understanding of the results of the company’s ongoing operations.

- Fee-related and other revenues grew 8 percent to $397 million compared to $366 million in the second quarter of 2024, which reflects a 19 percent increase in ancillary revenues, higher royalties and franchise fees, as well as higher pass-through revenues due to the company’s global franchisee conference in May.

- The company generated net income of $87 million, a 1 percent increase compared to the second quarter of 2024, as higher adjusted EBITDA and lower transaction-related expenses were partially offset by the absence of a benefit in connection with the reversal of a spin-off related matter, higher restructuring costs, and increased interest expense. Adjusted net income grew 13 percent to $103 million compared to $91 million in the second quarter of 2024.

- Adjusted EBITDA grew 10 percent to $195 million compared to $178 million in the second quarter of 2024. This increase included an $8 million favorable impact from marketing fund variability, excluding which adjusted EBITDA grew 5 percent on a comparable basis, primarily reflecting increased ancillary revenues, as well as higher royalties and franchise fees, partially offset by higher operating expenses primarily related to growth in the company’s credit card program and the absence of a benefit from insurance recoveries.

- Diluted earnings per share increased 6 percent to $13 compared to $1.07 in the second quarter of 2024. This increase primarily reflects the benefit of a lower share count due to share repurchase activity.

- Adjusted diluted EPS grew 18 percent to $1.33 compared to $1.13 in the second quarter of 2024. This increase included a favorable impact of $0.07 per share related to marketing fund variability (after estimated taxes). On a comparable basis, adjusted diluted EPS increased approximately 11 percent year-over-year, reflecting comparable adjusted EBITDA growth, the benefit of share repurchase activity, and lower depreciation and amortization, partially offset by higher interest expense.

- During the second quarter of 2025, the company’s marketing fund revenues exceeded expenses by $3 million; while in the second quarter of 2024, the company’s marketing fund expenses exceeded revenues by $5 million, resulting in $8 million of marketing fund variability.

Balance Sheet and Liquidity

The company generated $70 million of net cash provided by operating activities and $88 million of adjusted free cash flow in the second quarter of 2025. The company ended the quarter with a cash balance of $50 million and approximately $580 million in total liquidity.

The company’s net debt leverage ratio was 3.5 times as of June 30, 2025, the midpoint of the company’s 3 to 4 times stated target range, and in line with expectations.

Share Repurchases and Dividends

During the second quarter, the company repurchased approximately 923,000 shares of its common stock for $77 million.

The company paid common stock dividends of $32 million, or $0.41 per share, during the second quarter of 2025.

Full-Year 2025 Outlook

The company is increasing its adjusted diluted EPS outlook to reflect the impact of second-quarter share repurchase activity and increasing the low-end of its year-over-year rooms growth outlook by 40 basis points to reflect the removal of the dilutive impact from its Super 8 master licensee in China.

The company continues to expect marketing fund revenues to approximate expenses during full-year 2025, though seasonality of spend will affect the quarterly comparisons throughout the year.

Marriott International completed its $355 million acquisition of lifestyle hotel brand CitizenM, the company announced Wednesday.

The move brings 37 open hotels, or more than 8,700 rooms, into Marriott’s portfolio. Two more CitizenM hotels, totalling more than 300 rooms, are also in development.

“As travelers continue to seek innovative lodging offerings that blend technology with genuine, people-first hospitality, the citizenM brand is the perfect addition to our portfolio,” said Marriott President and CEO Anthony Capuano in a statement.

Plans for the acquisition were announced in April. Marriott now begins the process of integrating CitizenM hotels into its systems and platforms, according to the announcement. They will remain bookable via CitizenM platforms until the integration is complete, which Marriott expects to be later this year.

According to Marriott, there are “more details to come” about how CitizenM’s subscription program will work following integration, but the program is currently still live.

The CitizenM acquisition is part of Marriott’s broader strategy to build its select-service portfolio globally, per the announcement. In his statement, Capuano pointed to other select-service lifestyle brands the company is currently growing, including AC Hotels, Moxy and Aloft.

Earlier this week, Marriott opened its largest AC Hotel in North America in Arlington, Virginia, following a multimillion-dollar renovation of the former Crystal City Marriott.

Competition for talent and resources in the lifestyle space is heating up as hotel players expand in the increasingly popular segment, hospitality industry leaders told Hotel Dive earlier this year.

On the heels of the acquisition announcement, however, industry experts warned that Marriott would need to be wary of cannibalization as it integrates CitizenM into its portfolio of similarly positioned lifestyle brands, particularly Moxy.

Marriott CFO Leeny Oberg, however, told Hotel Dive in April that the company has “a proven track record of being able to acquire brands and then grow them as part of our overall system, but at the same time, preserving what makes them unique and attractive to the guests.”

The Federal Trade Commission granted Marriott approval for the CitizenM acquisition last month.

-

Brand Stories3 days ago

Brand Stories3 days agoBloom Hotels: A Modern Vision of Hospitality Redefining Travel

-

Brand Stories2 days ago

Brand Stories2 days agoOlive Living: India’s Intelligent, Community-Centric Hospitality Powerhouse

-

Destinations & Things To Do3 days ago

Destinations & Things To Do3 days agoUntouched Destinations: Stunning Hidden Gems You Must Visit

-

AI in Travel3 days ago

AI in Travel3 days agoAI Travel Revolution: Must-Have Guide to the Best Experience

-

Brand Stories3 weeks ago

Brand Stories3 weeks agoVoice AI Startup ElevenLabs Plans to Add Hubs Around the World

-

Brand Stories2 weeks ago

Brand Stories2 weeks agoHow Elon Musk’s rogue Grok chatbot became a cautionary AI tale

-

Asia Travel Pulse3 weeks ago

Asia Travel Pulse3 weeks agoLooking For Adventure In Asia? Here Are 7 Epic Destinations You Need To Experience At Least Once – Zee News

-

AI in Travel3 weeks ago

AI in Travel3 weeks ago‘Will AI take my job?’ A trip to a Beijing fortune-telling bar to see what lies ahead | China

-

Brand Stories3 weeks ago

Brand Stories3 weeks agoChatGPT — the last of the great romantics

-

The Travel Revolution of Our Era1 month ago

The Travel Revolution of Our Era1 month agoCheQin.ai Redefines Hotel Booking with Zero-Commission Model

You must be logged in to post a comment Login